Despite its importance, tax planning for doctors is often one of the last things on the minds of medical professionals. And understandably so, as most doctors focus on providing excellent patient care while staying abreast of advancements in medicine.

But when tax season arrives, doctors without strong systems in place often find the administrative stress detracts from their necessary focus on patients.

This article explores the importance of tax planning for doctors, lays out the foundations of the medical tax landscape, and then outlines strategies and solutions for effective tax planning.

The Importance of Tax Planning For Doctors

While for many doctors tax planning is considered an afterthought, the role it plays in healthy finances cannot be understated. Strong tax planning can help:

- Mitigate risk by avoiding penalties and interest for non-compliance with tax laws

- Manage cash flow effectively

- Identify new tax-saving opportunities

- Enable strategic investment for the practice

- Adjust tax planning strategies in response to legislative changes

- Maximize after-tax income

- Provide financial and retirement security for doctors’ families

Understanding the Landscape of Tax Planning for Doctors

Doctors face a unique tax landscape compared to many other businesses. Some key areas that medical practices must consider in their tax planning include:

- Treatment of healthcare benefits and reimbursements

- Special tax rules for healthcare investments and partnerships

- Credits and deductions specific to medical practices

- Tax treatment of different sources of income (e.g., salary, bonuses, self-employment income)

Effective Tax Planning Strategies for Doctors

Incorporating Tax-Efficient Business Structures

Different business entities have tax advantages and disadvantages, and choosing the best structure(s) for your practice will vary based on your practice’s goals and location.

Doctors may consider the following incorporation structures:

- Sole proprietorship

- Partnership between two or more practitioners

- Limited liability company (LLC)

- Corporation

- Physician cooperative

- Not-for-profit structures such as charities

When deciding on the best incorporation structure for your goals, consider:

- Liability protection

- Changing local, state, and national laws impacting each structure

- Potential tax savings through salary versus dividends

- Administration and reporting requirements

- Credibility of each structure from the perspective of patients and creditors

- Level of transparency required in the entity’s business finances

Special Considerations for Solo Practitioners vs. Group Practices

Whether you’re a solo practitioner or part of a group practice, understanding unique tax considerations is crucial for optimizing tax planning and ensuring compliance.

For solo practitioners, incorporation offers advantages such as lower rates and liability protection. Solo practitioners also benefit from specific deductions including home office expenses, self-employed health insurance deductions, and solo 401(k) contributions.

In group practices, doctors have opportunities for tax optimization through income splitting and partnership structures. By forming partnerships or professional corporations, doctors can strategically distribute income among partners or shareholders in a tax-efficient manner, maximizing overall tax outcomes for the group. Group practices can also benefit from specific deductions and benefits tailored to their structure, such as group healthcare plans.

Maximizing Deductions and Credits

Being aware of tax-saving opportunities can reduce your tax burden.

The first step is to ensure you are able to identify deductible expenses. Keep meticulous records of business expenses, including office rent, utilities, medical supplies, and professional association dues. Don’t forget to take advantage of deductions for home office expenses, travel, and meals related to business activities.

The next step is to be aware of common deductions and credits available to doctors, such as:

- Medical expenses deductions

- Continuing education and professional development expenses

- Qualified business income deduction (for eligible self-employed doctors)

- Health savings account (HSA) contributions

- Retirement plan contributions (e.g., 401(k), IRA)

Addressing Potential Pitfalls and Liabilities in Tax Planning for Doctors

Tax planning for doctors can come with many potential pitfalls, but when addressed proactively these can be confronted with confidence.

Some simple strategies to mitigate potential pitfalls include:

- Maintaining accurate and up-to-date financial records to support tax deductions and credits claimed on your tax return.

- Implementing internal controls and compliance procedures to minimize the risk of tax audits and penalties which are re-visited regularly.

- Consulting with professionals specializing in tax planning for doctors, who can provide proactive insights and help with changing legislation.

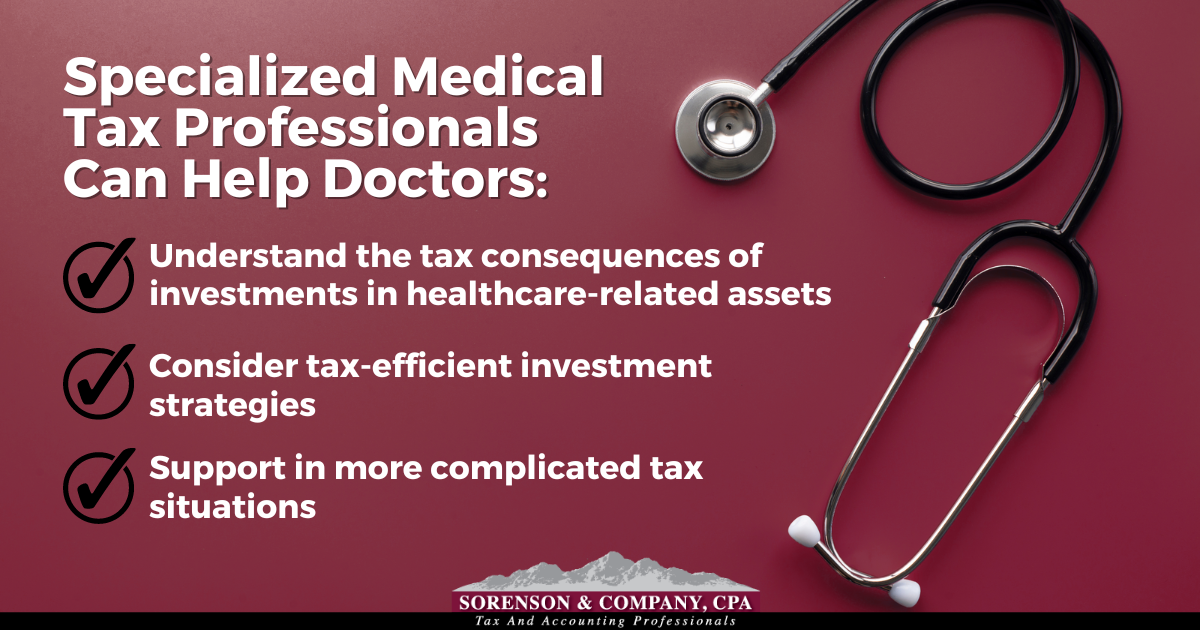

Specialized medical tax professionals can go far beyond filing your taxes. They can help doctors:

- Understand the tax consequences of investments in healthcare-related assets, such as medical equipment, real estate, or technology.

- Consider tax-efficient investment strategies, such as depreciation deductions and capital gains deferral, when acquiring and disposing of healthcare assets.

- Support in more complicated tax situations, such as doctors who practice in multiple states or offer telemedicine services which may be subject to different taxes in each jurisdiction.

Wealth Management and Long-Term Tax Planning for Doctors

Long-term tax planning and wealth management are critical aspects of a doctor’s financial strategy. Consider investing in tax-advantaged accounts with benefits such as tax-deferred growth or tax-free withdrawals in retirement, allowing you to maximize investment returns while reducing current tax burdens.

Consider investing in accounts such as:

- Individual retirement accounts (IRAs)

- Roth IRAs

- Employer-sponsored retirement plans like 401(k)s.

As part of estate planning, doctors should also consider tax-efficient asset transfer mechanisms. Techniques such as establishing trusts, including irrevocable life insurance trusts (ILITs) and charitable remainder trusts (CRTs), can minimize estate taxes and facilitate the transfer of your assets to beneficiaries.

Professionals with a Focus in Tax Planning for Doctors

Navigating tax planning can be time-consuming, but by choosing experts to support your practice, you’ll save time and be able to approach tax planning with confidence.

When choosing a tax advisor for your medical practice, look for professionals with a track record of working with healthcare professionals, who hold relevant certifications such as CPAs. Without this expertise, changes in relevant legislation, deductions, and credits might be overlooked.

At Sorenson & Company, CPA, we know how to find little-known tax deductions, hidden loopholes, and proven strategies that help our medical clients save thousands each year. Our team’s experience spans a variety of jurisdictions, ensuring your practice will comfortably navigate state and national tax requirements, regardless of the incorporation structure you choose.

Contact us today, we’re here to help!